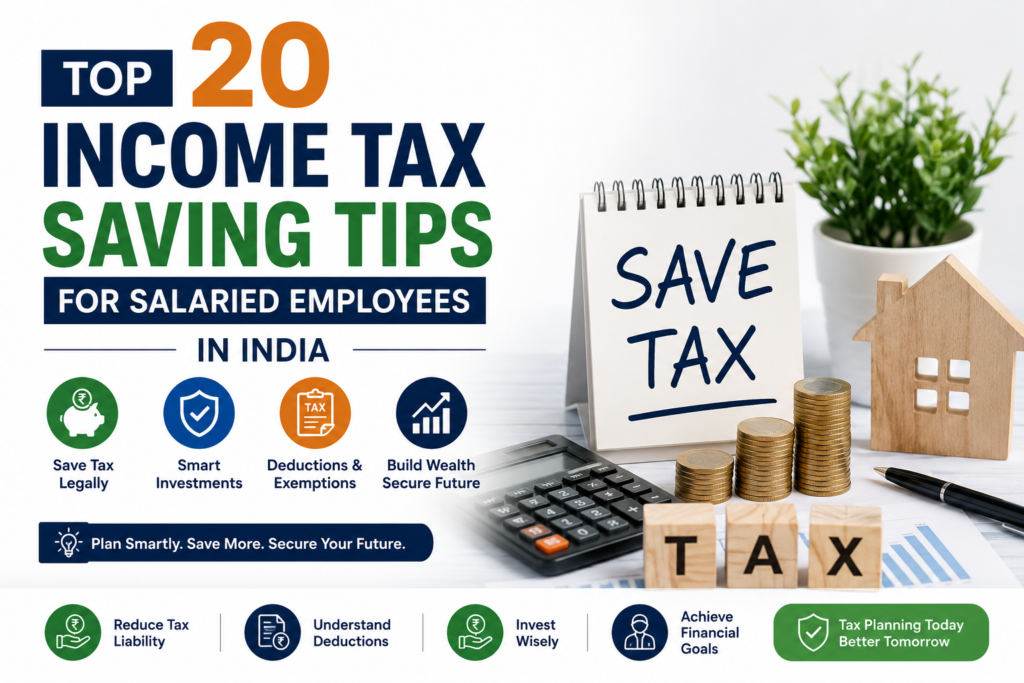

Top 20 Income Tax Saving Tips for Salaried Employees in India (2026 Guide)

Paying income tax is an important financial responsibility, but paying more tax than necessary is not. With proper income tax planning, salaried employees in India can legally reduce their tax liability while building long-term wealth. Understanding the available deductions, exemptions, and investment options under the Income Tax Act can help you maximize your savings.

In this comprehensive guide, we’ll explore the top 20 income tax saving tips for salaried employees that can help you make informed financial decisions during the financial year.

Why Income Tax Planning is Important

Effective tax planning offers several benefits:

Reduces your overall tax liability

- Increases your annual savings

- Helps achieve long-term financial goals

- Encourages disciplined investing

- Ensures compliance with tax laws

- Avoids penalties and interest on late filings

The key is to start planning early instead of rushing at the end of the financial year.

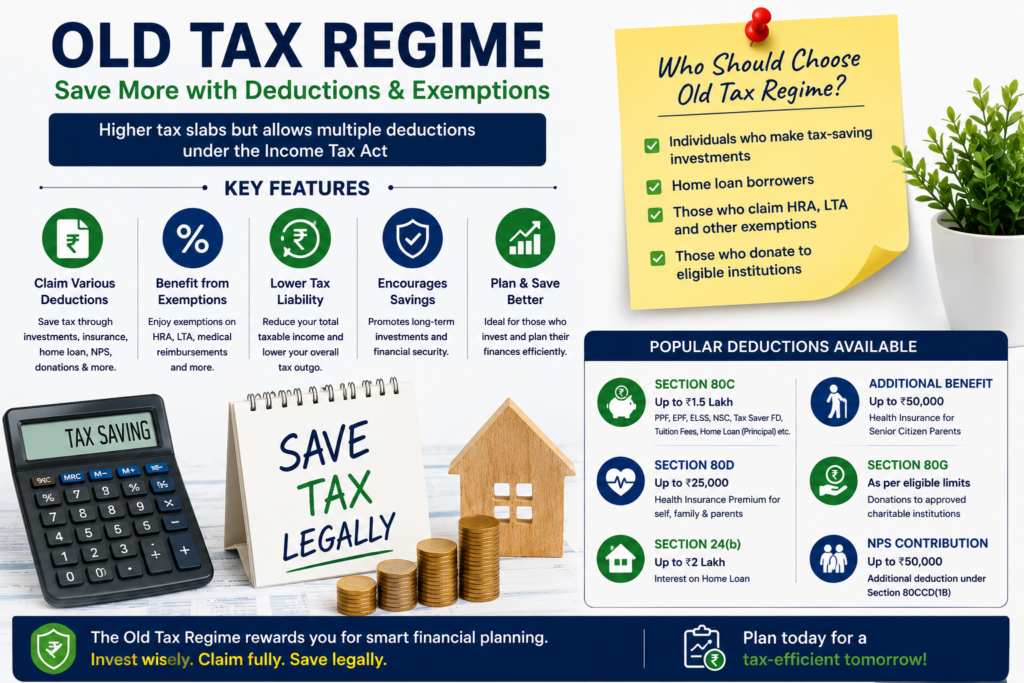

1. Compare the Old and New Tax Regime

One of the first decisions every salaried employee should make is selecting the appropriate tax regime.

Old Tax Regime

The old regime allows taxpayers to claim various deductions and exemptions, such as:

Section 80C investments

Health insurance deductions

House Rent Allowance (HRA)

Home loan benefits

Leave Travel Allowance (LTA)

New Tax Regime

The new regime offers lower tax rates but allows fewer deductions and exemptions.

Tip: Calculate your tax liability under both regimes before making your choice.

2. Maximize Section 80C Investments

Section 80C remains one of the most popular ways to save income tax.

Eligible investments include:

![]() Employees’ Provident Fund (EPF)

Employees’ Provident Fund (EPF)

Public Provident Fund (PPF)

Public Provident Fund (PPF)

Equity Linked Savings Scheme (ELSS)

Equity Linked Savings Scheme (ELSS)

National Savings Certificate (NSC)

National Savings Certificate (NSC)

Tax Saver Fixed Deposits

Tax Saver Fixed Deposits

![]() Sukanya Samriddhi Yojana

Sukanya Samriddhi Yojana

Children’s Tuition Fees

Children’s Tuition Fees

Home Loan Principal Repayment

Home Loan Principal Repayment

Planning these investments throughout the year helps avoid financial pressure in March.

3. Claim Health Insurance Benefits Under Section 80D

Health insurance protects your family while providing valuable tax benefits.

You can claim deductions for:

Spouse

Spouse

Parents

Parents

Children

Children

MySelf

MySelf

Premiums paid for senior citizen parents generally qualify for higher deduction limits under applicable tax rules.

4. Claim House Rent Allowance (HRA)

If you receive HRA and live in rented accommodation, you may be eligible for tax exemption.

Keep the following documents ready:

![]()

Rent receipts

Rental agreement

Landlord’s PAN (where applicable)

Proper documentation is essential during tax filing.

5. Claim Home Loan Tax Benefits

Buying a home can significantly reduce your tax liability.

You may claim deductions on:

- Home loan principal repayment

- Home loan interest

- Additional benefits for eligible first-time buyers under applicable provisions

6. Invest in National Pension System (NPS)

NPS is an excellent retirement planning tool that also provides additional tax-saving opportunities under the Income Tax Act.

Benefits include:

- Retirement corpus creation

- Potential tax savings

- Long-term wealth accumulation

7. Utilize Leave Travel Allowance (LTA)

Employees receiving Leave Travel Allowance can claim tax exemption on eligible domestic travel expenses.

Remember to retain:

- Air or train tickets

- Hotel invoices (where relevant)

- Travel proof

8. Claim Standard Deduction

Eligible salaried employees can claim the standard deduction available under current tax provisions. This deduction automatically reduces taxable salary without requiring any investment.

9. Claim Education Loan Interest

Interest paid on eligible education loans for higher education qualifies for tax deductions. This benefit applies to loans taken for yourself, your spouse, children, or a legal ward, subject to applicable conditions.

10. Claim Deductions for Charitable Donations

Donations made to approved charitable institutions may qualify for deductions under Section 80G.

Always request:

- Donation receipt

- Registration details of the organization

11. Make Full Use of Employer Allowances

Depending on your salary structure, you may receive reimbursements for:

- Telephone expenses

- Internet bills

- Official travel

- Professional development

Review your salary package with your HR department.

12. Invest Early Instead of Waiting Until March

Investing early offers multiple advantages:

- Better investment returns

- Monthly financial discipline

- Reduced year-end stress

- Improved cash flow

Waiting until the last month often leads to poor investment decisions.

13. Organize Your Tax Documents

Maintain a dedicated folder containing:

- Form 16

- Investment proofs

- Insurance receipts

- Home loan certificate

- Rent receipts

- Donation receipts

Organized records make tax filing easier and reduce errors.

14. Verify Form 16, AIS and Form 26AS

Before filing your Income Tax Return (ITR):

- Verify salary details

- Check TDS deductions

- Confirm investment entries

- Match information with AIS and Form 26AS

Any mismatch should be corrected before filing.

15. File Your Income Tax Return Before the Due Date

Timely filing offers benefits such as:

- Faster refunds

- Better credit profile

- Easier visa processing

- Hassle-free loan approvals

Late filing may result in penalties and interest.

16. Invest in ELSS Mutual Funds

ELSS funds are among the most popular tax-saving investment options.

Advantages include:

- Tax deduction eligibility

- Wealth creation potential

- Short lock-in period

- Equity market growth opportunities

17. Optimize Your Salary Structure

Discuss tax-efficient salary components with your employer.

A well-designed compensation package can include eligible reimbursements and allowances that help improve tax efficiency while remaining compliant with applicable laws.

18. Plan Capital Gains Carefully

If you invest in:

- Stocks

- Mutual funds

- Real estate

- Gold

Understand how capital gains are taxed. Strategic planning can help optimize your tax liability within legal limits.

19. Consult a Professional Tax Advisor

Tax laws evolve regularly.

Professional tax consultants can help you:

- Select the right tax regime

- Maximize eligible deductions

- File accurate returns

- Handle tax notices

- Plan investments strategically

Expert advice often saves more than it costs.

20. Make Tax Planning a Year-Round Habit

The best tax-saving strategy is consistent planning.

Create an annual financial roadmap covering:

- Investments

- Insurance

- Retirement planning

- Emergency savings

- Home loan planning

- Tax-saving goals

Tax planning should be part of your monthly financial routine—not just a year-end activity.

Common Tax Saving Mistakes to Avoid

Avoid these common errors:

- Waiting until the financial year-end to invest

- Ignoring available deductions

- Choosing the wrong tax regime

- Filing incorrect information

- Forgetting to verify Form 16

- Missing the ITR deadline

- Losing important tax documents

Proper planning can help you avoid unnecessary taxes and penalties.

Frequently Asked Questions (FAQs)

Which tax regime is better for salaried employees?

The answer depends on your income, eligible deductions, and financial goals. Compare your tax liability under both regimes before deciding.

What are the best tax-saving investments?

Popular options include EPF, PPF, ELSS, NPS, tax-saving fixed deposits, and eligible life insurance policies, depending on your financial objectives.

Is health insurance tax deductible?

Yes. Eligible health insurance premiums may qualify for deductions under Section 80D, subject to the applicable provisions and limits.

Can I claim HRA if I live in a rented house?

If you receive House Rent Allowance and meet the eligibility conditions, you may claim an HRA exemption by maintaining the required documentation.

Should I hire a tax consultant?

If you have multiple income sources, investments, capital gains, rental income, or business income, consulting a tax professional can help ensure compliance and optimize your tax planning.

Conclusion

Smart income tax planning is one of the most effective ways for salaried employees to improve their financial health. By understanding the available deductions, exemptions, and investment options, you can legally reduce your tax burden while achieving your long-term financial goals.

Start planning at the beginning of the financial year, maintain proper documentation, and review your tax strategy regularly. If your financial situation becomes more complex, seeking professional guidance can help you stay compliant and make the most of the tax-saving opportunities available under the law.

Whether you’re a first-time taxpayer or an experienced professional, following these 20 income tax saving tips can help you build a stronger financial future while minimizing your tax liability.

Need Expert Tax Assistance?

Our team of experienced tax professionals provides:

- Income Tax Return (ITR) Filing

- Tax Planning & Advisory

- GST Registration & Return Filing

- Accounting & Bookkeeping

- Payroll Management

- Business Registration

- Virtual CFO Services

- Financial Advisory

Contact us today to simplify your tax planning and stay compliant with confidence.